2020 Outlook: What Could Possibly Go Wrong?

Slowing economic growth increases uncertainty after a golden year for financial assets

By Crescent Team

Our 2020 outlook steps off the shoulders of 2019, a year in which several asset classes hit new all-time highs and valuations are approaching similarly full levels. Investors are looking to 2020 and asking if trade wars, or even war, will finally derail markets moving higher, will a contentious election prove impactful in the U.S. or does the Fed’s more accommodate reversal in 2019 mean we’re back to the races?

In the sections following, we break down the primary drivers to asset prices, discuss our updated outlook for long-term returns and pull out key themes investors should consider in 2020.

CAPITAL MARKET FACTORS

Economic Growth

While accommodative monetary policy, a “phase one” U.S.-China trade deal and transparency on Brexit provide some clarity heading into 2020, global business activity ended 2019 on a weak note. We will continue to monitor an ensemble of macroeconomic data, but acknowledge that a slower growth trajectory may limit prospects for incrementally higher financial asset valuations. Therefore, we favor a defensive portfolio stance with a greater focus on managing risk exposure than reaching for return targets.

Monetary policy

Investors will remember 2019 as the year Fed officials embraced the power of its balance sheet to achieve policy goals. After shrinking its balance sheet by more than $692 billion over two years through August 2019, the Fed added more than $405 billion in just the final four months of 2019 and forecast balance sheet expansion in 2020. In our view, increased global growth uncertainty heading in 2020 strengthens the case for incremental monetary policy accommodation in the form of lower rates and even more balance sheet expansion. Relative to Gross Domestic Product (GDP), the Fed has significantly more room to grow its balance sheet in 2020, which may support financial asset valuations and prolong the business cycle.

Fiscal

Monetary policy impotence and sluggish growth may be the catalysts for meaningful discourse on fiscal reforms and modern monetary theory (MMT) in the U.S., Euro Area and developed markets. However, meaningful progress will take time and is unlikely to boost household consumption in 2020.

Inflation

Through November, the Fed’s preferred year-over-year inflation measure, core personal consumption expenditure price index (“PCE”), remained stubbornly low at just 1.6 percent. Although long-term broad inflation expectations remain well-anchored, any upside inflation surprise should support equity valuations and inflation-sensitive bonds, such as Treasury Inflation-Protected Securities (TIPS).

Currency

The trade-weighted U.S. dollar ended 2019 near 20-year highs despite the Fed’s mid-year dovish pivot and asset purchase program reboot beginning in September 2019 dubbed “not-quantitative easing” (not-QE). Although Fed policy may not spur consumption growth, it may successfully weaken the U.S. dollar relative to foreign currencies and boost valuations for tangible assets and international equities.

CRESCENT WEALTH ADVISORY 10-YEAR CAPITAL MARKET ASSUMPTIONS

2019 was a golden year for financial asset returns characterized by falling interest rates, narrowing credit spreads and rising global equity valuations, meaning it was good to be invested. However, prospectively, investors have to leave 2019 in the past and consider what lies ahead. The table below summarizes our 10-year outlook and it is a rare showing of negative year-over-year changes for all asset classes listed. The primary driver is elevated valuations across assets classes. In particular, the Federal Open Market Committee (FOMC) cut interest rates three times in 2019, drove bond prices higher and subsequently reduced our return expectations on across fixed income.

Strong global equity returns, driven by elevated valuations, pulled future return expectations forward. Consequently, our global equity return forecasts fell 50 to 60 basis points. Such consistency within global fixed income and global equities, respectively, is a first in the history of our capital market process.

While return expectations for real assets and alternatives also fell year over year, our 10-year return forecast for midstream energy remains elevated relative to other asset classes. Changes to hedge fund and private equity forecasts are tangential to changes in public fixed income and equity return assumptions.

INVESTMENT THEMES FOR 2020

In our view, financial market conditions entering 2020 favor a greater emphasis on risk management over striving to achieve return targets. While our base case today, markets are dynamic and we will update our base-case expectations as financial market conditions evolve. Our latest 10-year capital market forecasts call for a lower return outlook relative to prior years for stated volatility targets. As such, we recommend incorporating these themes into your investment process to mitigate return-reaching portfolios and manage risk-taking.

1. Managing Risk > Targeting Return

Key Observation Beginning 2020 – Incrementally weak manufacturing and household data suggest the U.S. economy may be approaching the late stages of its business cycle. Meanwhile, the manufacturing sector in Europe remains weak and emerging markets are grappling with a secular slowdown in China and slower global growth.

Global Markit IHS PMI Composite data indicates global growth trends, while positive, remain weak. Furthermore, U.S. Industrial Production growth, a key measure of output from businesses in the industrial sector, turned negative in September and remained in contractionary territory through November (December data not yet released). Since 1948, industrial production contracted 14 times. 13 of those instances occurred just before, or during, a recession. The period from April 2015 to November 2016 was the only exception.

Adding to our cautionary stance on U.S. growth, personal consumption expenditures slowed over the course of 2019 despite the unemployment rate near 50-year lows and steady wage growth.

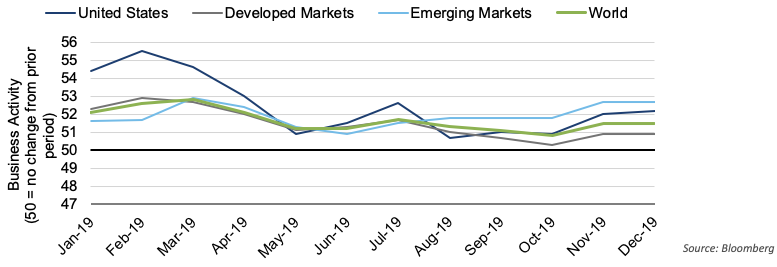

Business Activity Remains Sluggish

Global PMI Composite trends show business conditions slowed through 2019, strengthening the case for fiscal or monetary policy accommodation if the trend persists.

Industrial Production Growth Contracts

Year-over-year declines in the Industrial Production Index always coincided, or just preceded, a recession (grey bars).

Portfolio Impact

The strong rebound in equity valuations following the fourth quarter sell-off in 2018 may have run its course. We believe weak business activity and slower U.S. household consumption growth present fundamental challenges for incremental equity valuation expansion. Therefore, we caution against reaching for return and favor reassessing total portfolio risk tolerances.

2. (Corporate) Credit Check

Key Observation Beginning 2020 – Another late-cycle trend, credit stress, emerged in the second half of 2019 despite three Fed rate cuts and a “not-QE” reboot. Specifically, credit spreads on CCC-rated corporate debt drifted higher, indicating lower prices while spreads on BB- and B-rated corporate credit held steady. Last year we highlighted that lower-quality corporate bonds within the investment-grade market constituted a greater percentage than the rest of the investment-grade market combined. We believe this may limit the protection investment-grade bonds could provide in a down market. While this is largely still the case today, investment-grade bond spreads declined in response to the Fed’s dovish monetary policy pivot and balance sheet expansion program. However, the CCC-rated credit segment of the credit market appears unwilling to be tamed by monetary policy accommodation, which may signal additional unrest.

High Yield Spread Over Treasuries

We believe the divergence of CCC-rated corporate debt signals a potential shift in investor risk sentiment and bears watching.

BBB-Rated Corporate Debt Growth

Portfolio impact – More tempered allocations to credit and thoughtful utilization of active bond managers, especially within high yield bonds, to navigate the level of quality in today’s market are prudent adjustments.

3. A Case for Global Equity Exposure

Key Observation Beginning 2020 – U.S. stocks once again led the rebound in global equities despite relatively more attractive valuations on international equities at the beginning of 2019. In fact, despite carrying a relatively elevated valuation each year, the S&P 500 Index outperformed the MSCI EAFE Index in seven of the last 10 calendar years! Since 1978 however, the S&P 500 Index outperformed the MSCI EAFE Index in just 22 of the last 42 (52 percent) calendar years. Furthermore, our research shows relative performance between domestic and international equities is cyclical and influenced by U.S. dollar strength (or weakness) relative to major currencies. While valuations are observable and measurable, currency fluctuations are difficult to predict. Therefore, given international equities have relatively more favorable valuations and the prospect that U.S. dollar strength may abate, we continue to recommend global equity diversification.

Foreign Currency Effects

U.S. dollar fluctuations are cyclical and play a role in relative performance trends between domestic and international equities.

Portfolio impact – We continue to recommend strategic allocations to international developed and emerging market equities to take advantage of opportunities outside of the U.S.

For more information, please contact any of the professionals at Crescent Wealth Advisory.

Download a PDF version of this post.