Rally Continued, but Paced Slowed

Mixed style factor performance, inflation risks remained low

By Crescent Team

KEY OBSERVATIONS

The rebound in global assets continued in August, led by U.S. large cap equities, but value showed signs of life in Europe and China pulled emerging market equities into positive territory year-to-date.

Sustained upside inflation risks remain low despite recent stimulus measures, but inflation dynamics are fluid.

We encourage investors to keep their investment horizon in focus and not allow emotions to influence portfolio positioning.

MARKET RECAP

Expectations that U.S. policymakers would complement ultra-accommodative monetary policy with additional fiscal stimulus extended the rebound in global risk assets through August. Large-cap technology stocks led the U.S. rally again with notable returns from Apple (+18.7 percent) and Amazon (+10.8 percent), lifting the S&P 500 Index 7.2 percent in August. Although small-cap stocks trailed their large-cap counterparts, the Russell 2000 Index ended 5.6 percent higher. While growth continued to lead value stocks within domestic equities, small-cap value stocks led the rally within international developed stocks and lifted the MSCI EAFE Index 5.1 percent. The MSCI Emerging Market Index rallied 2.2 percent, led by a 4.4 percent return on Chinese equities, and ended August in positive territory year to date.

Global fixed income returns were relatively muted in August. Treasury yields rose slightly, and credit spreads narrowed. Consequently, Core U.S. bonds fell 0.8 percent, and U.S. High Yield gained 1 percent. TIPS returned 1.1 percent and benefited from higher inflation expectations and the Fed’s commitment to keeping rates low until inflation sustainably exceeds its 2 percent target.

Real assets, namely commodities, benefited from a weaker U.S. dollar (-1.3 percent in August). However, returns on REITs and MLPs were just 0.8 percent and 0.5 percent, respectively, as reopening risks emerged.

INFLATION CONDITIONS

Following a series of fiscal and monetary policy measures to support economic growth, some market participants are wondering if inflation is poised to rise significantly in the near term and how to protect one’s portfolio. In our view, a sharp sustainable uptick in inflation seems unlikely at this time. However, we believe that inflation conditions are dynamic and both the line between Federal Reserve lending and spending is thinning. At the same time, fiscal policymakers appear willing to pass another round of stimulus. Therefore, we will continue to monitor policy for signals of rising inflation risks. In short, we hold the view that what policymakers say has less impact on longer-term inflation expectations than what they do.

Although CPI is higher year-over-year, it’s well below recent trends despite the magnitude of monetary and fiscal stimulus.

Contrary to a popular narrative, recent history shows increased money supply coincided with lower year-over-year CPI growth rates.

The CARES Act included a provision to provide the Fed with $454 billion to fund its lending facilities. On March 26, Fed President Jerome Powell appeared on NBC’s TODAY show and stated, “When it comes to this lending, we’re not going to run out of ammunition, that doesn’t happen.” What Powell said rang an inflationary tone. However, what the Fed did was less inflationary. Through July, it had not used 76 percent of the funds earmarked for its facilities.

During his press conference following the July FOMC meeting, a reporter asked Powell why utilization was lower than expected. He replied, “market participants, anticipating that the Fed would backstop risk assets, stepped in to purchase securities in those markets.” In short, the Fed achieved its policy objective (financial market stability) with words, not actions.

The fiscal policy response was also swift and substantial in magnitude. Elected officials cast partisan politics aside and sent needed liquidity to fill the shortfall left by lost sales revenue and wages as a result of COVID-19 containment measures. As a result, the second quarter fiscal deficit was $2.2 trillion and added to inflationary concerns. However, our analysis revealed that the private sector experienced a liquidity shortfall of approximately $600 billion during the second quarter, inclusive of fiscal and monetary stimulus. Since consumption represents about two-thirds of GDP growth, the liquidity shortfall experienced by the private sector will likely reduce spending power. It may also limit the ability to service debt obligations. In our view, delinquencies and default rates may rise and further weigh on consumption and CPI inflation if private sector liquidity conditions tighten too much.

The private sector economic shortfall during the second quarter may limit future consumption growth and the ability to service debt payments.

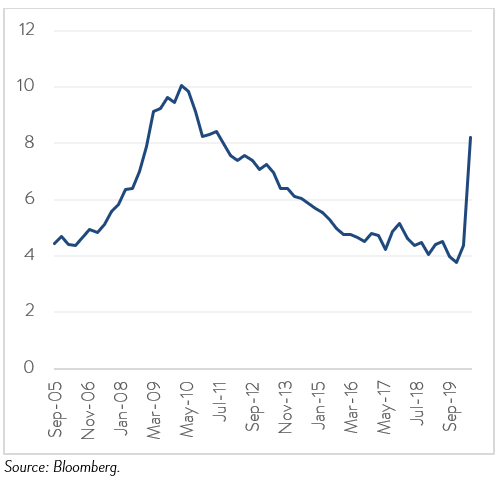

Mortgage delinquencies as a percent of total mortgages outstanding reached 8.2 percent in July, underscoring tight financial conditions.

In short, inflation is difficult to predict, but government policies and private sector financial conditions offer directional clues. As long as household and business conditions remain tight, we believe deleveraging and lower consumption trends are likely to persist in the near term. Our inflation outlook will hinge on these dynamics, government policy and the speed of economic recovery.

MARKET OUTLOOK

From an asset allocation perspective, we continue to update and evaluate our capital market assumptions and assess the implications for our client’s portfolios. In the absence of any changes in objectives or cash needs, we advocate for maintaining the established strategic asset allocation that’s rooted in fundamentals. Timing markets correctly is very challenging, especially in today’s environment. We encourage investors to keep their investment horizon in focus and not allow emotions to influence portfolio positioning.

For more information, please contact any of the professionals at Crescent Wealth Advisory.

Download a PDF version of this blog.

Note: This report is intended for the exclusive use of clients or prospective clients of Crescent Wealth Advisory. Content is privileged and confidential. Any dissemination or distribution is strictly prohibited. Information has been obtained from a variety of sources believed to be reliable though not independently verified. Any forecast represent future expectations and actual returns, volatilities and correlations will differ from forecasts. Past performance does not indicate future performance. The information presented does not represent a specific investment recommendation. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice.